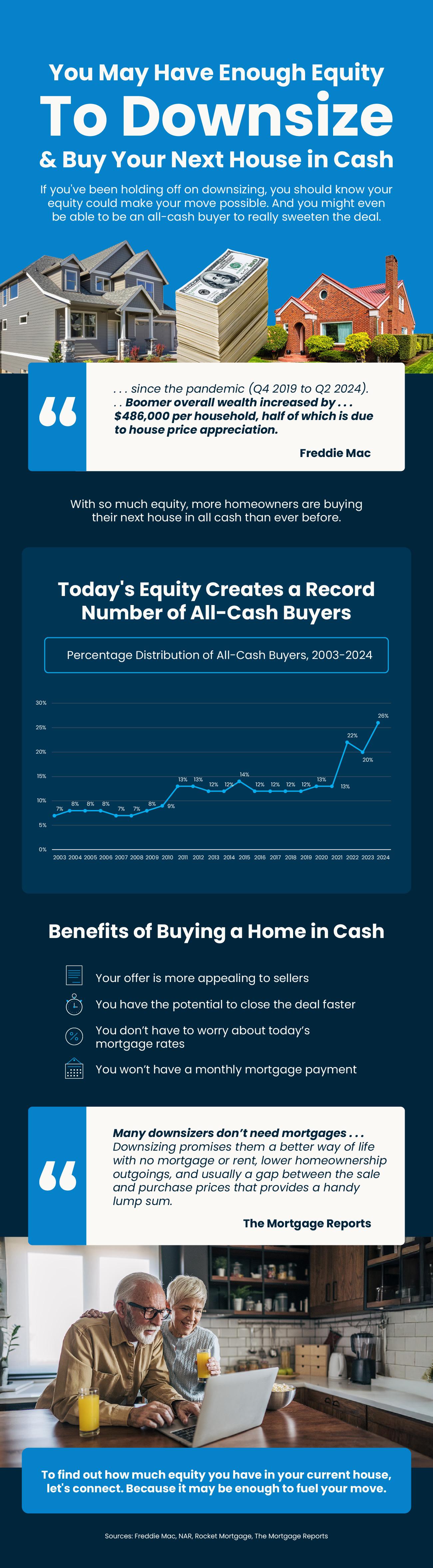

Have you been holding off on downsizing? If so, you should know your equity could make your move possible.

Homeowners today have so much equity that a record number are buying their next house in all cash. And that has some big benefits like making their offer more appealing, potentially closing faster, and not having a mortgage payment.

To find out how much equity you have in your current house, connect with a local agent. Because it may be enough to fuel your move.

When your house doesn’t sell, it doesn’t just feel frustrating – it feels personal. You put time, money, and emotional energy into this move. You told your friends and family it was happening. And now that your listing has expired without a buyer? You’re left feeling stuck, and maybe even a little embarrassed.

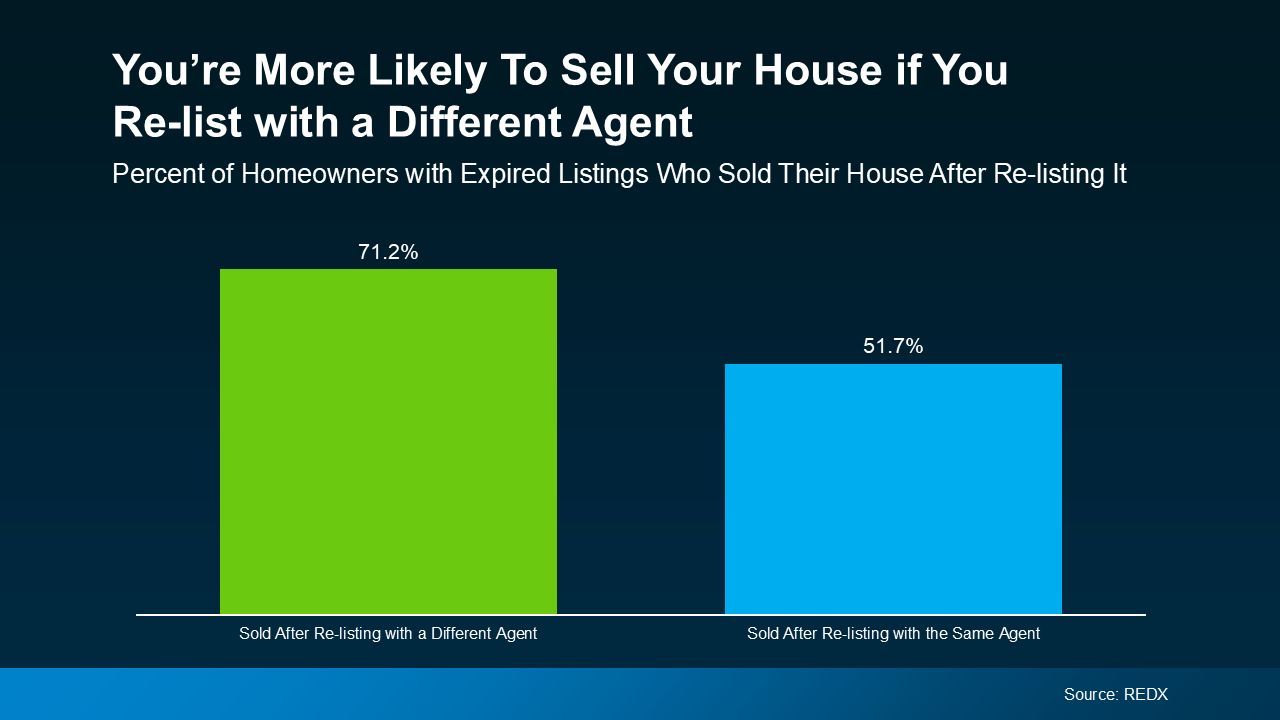

And here’s what most agents won’t tell you. Over 70% of homeowners who re-list with a different agent sell their house.

Re-list with the same agent? That stat drops to only 50%, according to the latest data from REDX. That’s like leaving the fate of your sale to a coin toss. And that’s not good enough.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better.

Same house. Different strategy. Completely different results.

Let’s break down what might’ve gone wrong – and how a fresh perspective can help you have a winning strategy this time.

1. It Was Priced Too High

Today, homebuyers are feeling the squeeze of higher mortgage rates, so even a slightly overpriced home will get overlooked. And once your listing starts to go stale, it’s hard to regain momentum.

Missing the mark on pricing is a costly mistake – and too many homeowners are doing that very thing right now.

What we need to do now: We need to analyze the latest sales in your area to make sure you’re hitting the right number. This includes taking a hard look at real-time buyer behavior, and any feedback you got from open houses or showings your first time around. Pricing at, or even just below, current market value is a winning play because it drives more buyers to your listing – and that amps up the competition for your home.

2. It Didn’t Show Well

You only get one shot at a first impression. If the listing photos didn’t pop, the house wasn’t staged well, or it wasn’t updated, most buyers will skip over it without ever scheduling a showing. And even if buyers did show up, small things like scuffed walls, outdated light fixtures, or a wobbly doorknob can turn them away.

What we need to do now: Let’s walk through your house withfresh eyes to see if there are any areas that may have been sticking points inside and out. Sometimes taking down old drapery, some light staging, or even a fresh coat of paint can completely change how a buyer feels about the home.

3. It Didn’t Get the Right Exposure

If your home didn’t sell, chances are it wasn’t getting the visibility it deserved. Generic flyers and a few online photos aren’t enough anymore. Today’s top agents are using highly targeted digital marketing, social media strategies, custom video content, and more to get your listing in front of the right buyers at the right time.

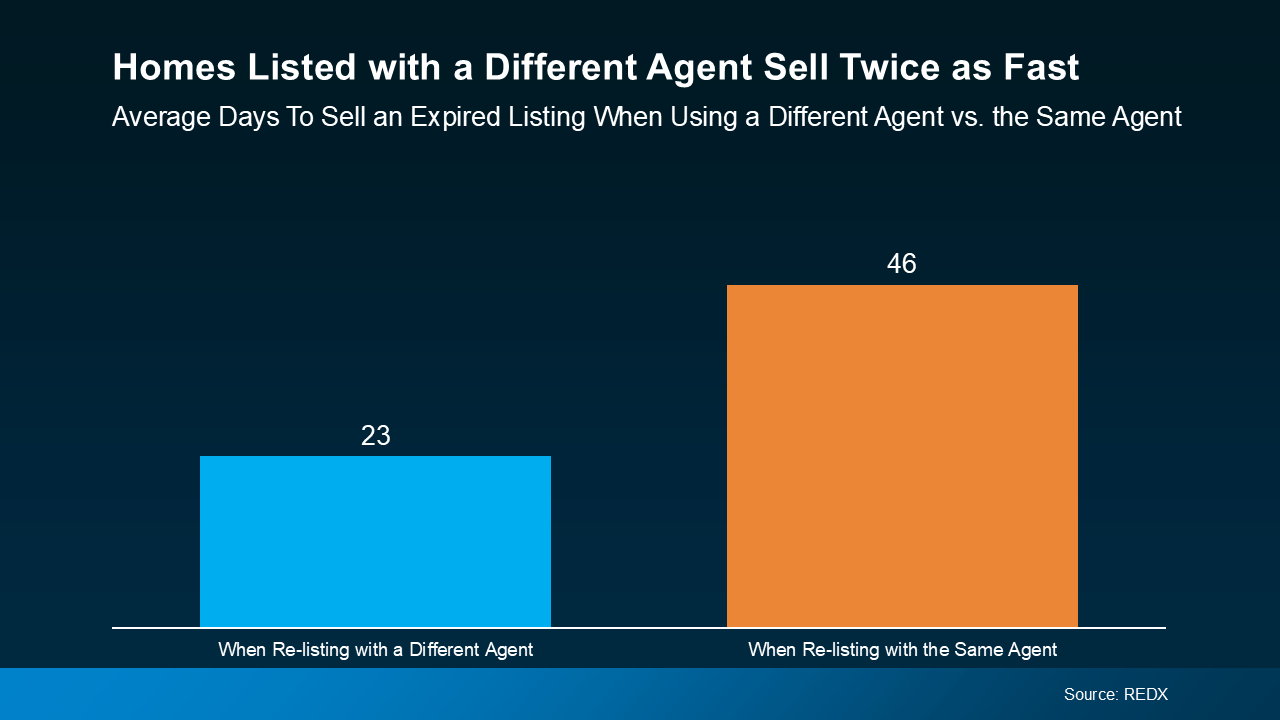

What we need to do now: We have to do more than just put your house online and hope it sells. Together, we can come up with a real plan to maximize its exposure. With the right pricing, staging, and marketing, your house will sell quickly. Here’s a real-world example (see graph below):

4. You Weren’t Willing To Negotiate

In this market, sellers who aren’t open to negotiating on things like closing costs, inspection repairs, or other concessions are often left behind. And if your last agent didn’t set that expectation with you, that’s a real shame.

What we need to do now: Be willing to meet buyers where they are. The goal is to get the deal done – and sometimes that means getting creative to help buyers cross the finish line. Home values have increased by over 55% over the last five years, so you likely have enough wiggle room to offer some perks without sacrificing your bottom line.

Bottom Line

If your house didn’t sell and your listing has expired, you don’t need to give up. You just need a better plan. And maybe, a better partner.

Over 70% of homeowners who switch agents sell their house the second time. That’s not a coincidence. That’s strategy.

If you’re ready for a proven approach, talk to a local agent so you know what to do differently – and why doing different things actually works. It’s time to get your move back on track.

After years of it feeling almost impossible to find a home you want to buy, things are changing for the better.

Nationally, inventory is growing, and that gives you more options for your move. But here’s what you need to know. That level of growth is going to vary based on where you live. And that’s why you need an agent’s local market expertise.

Here’s a quick rundown of the current inventory situation, so you know what’s happening and what to expect.

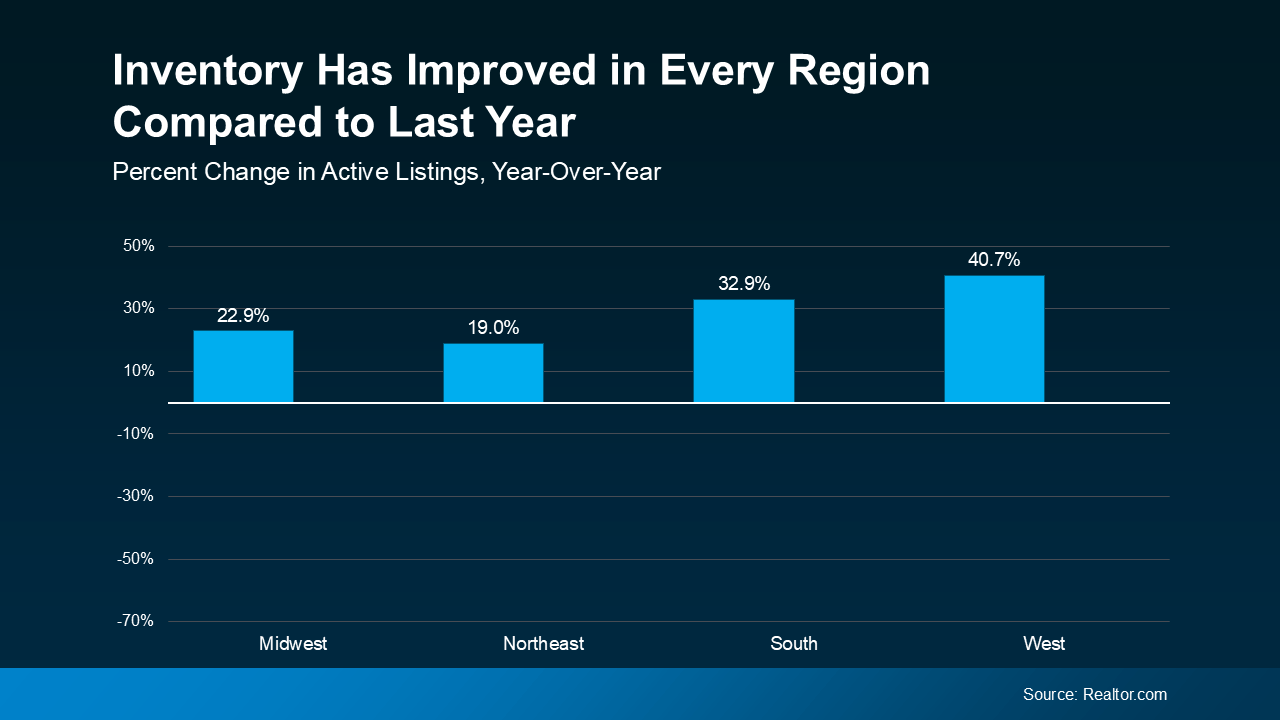

Significant Growth Across the Nation

Nationally, the number of homes for sale is rising – and that’s true in all regions of the country. That’s shown in this data from Realtor.com. In each of the four regions, inventory is up at least 19% compared to the same time last year. In the West, it’s actually up almost 41% year-over-year (see graph below):

There are two main reasons for this increase:

More sellers are listing their homes. Many homeowners have been waiting for mortgage rates to drop before making a move. Now, some have decided they can’t wait any longer. May had more new listings than any May in the past three years.

Homes are taking longer to sell. That means listings are staying on the market longer, which increases the total number of homes available. In May, the typical home took 51 days to sell – much closer to what’s more typical for the market.

More homes for sale helps the market become more balanced. For the past few years, sellers have had the upper hand. Now, things are shifting. Nationally, it’s not a full-on buyer’s market yet, but it’s heading toward a healthier place, especially for homebuyers. Danielle Hale, Chief Economist at Realtor.com, explains:

“The number of homes for sale is rising in many markets, giving shoppers more choices than they’ve had in years . . . the market is starting to rebalance.”

How Much Growth We’ve Seen Varies by Area

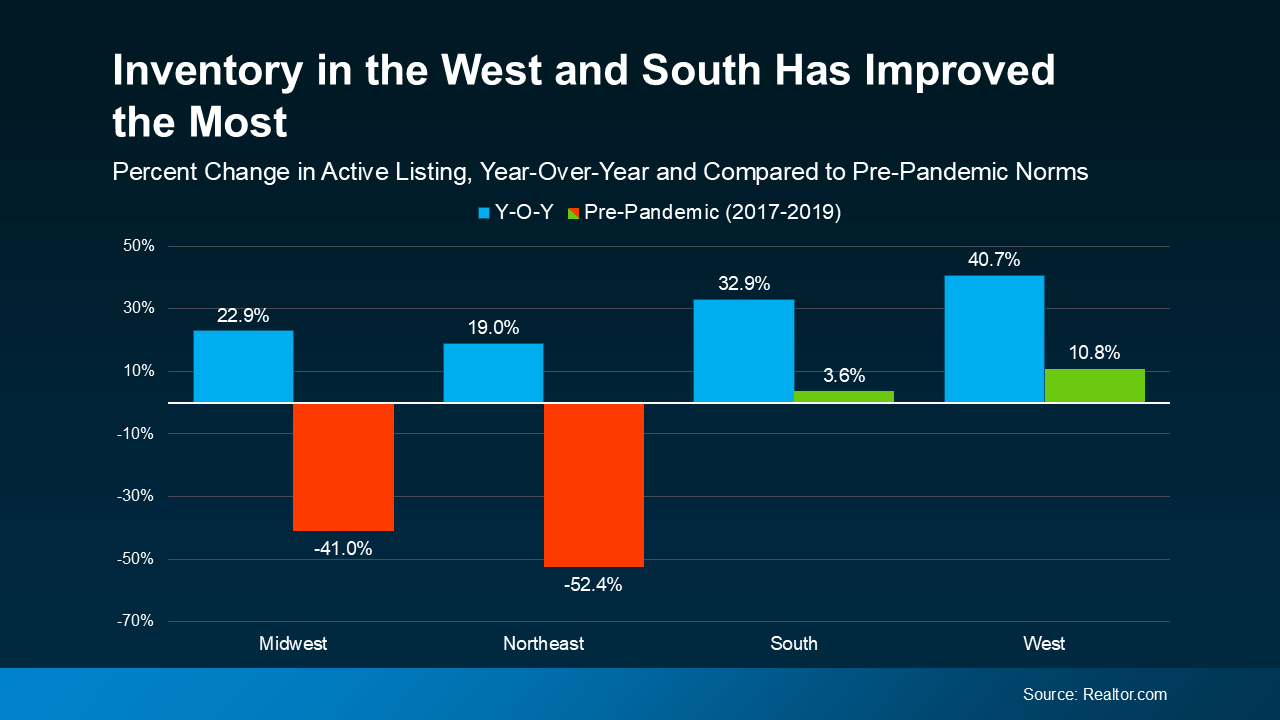

But, how long it’s going to take to achieve true balance is going to vary by area. Some parts of the country are seeing inventory bounce all the way back to normal levels, while others haven’t grown quite that much yet.

Let’s take a look at another graph. This time, we’ll compare the current data (what you already saw) to the last normal years in the housing market (2017-2019).

In this comparison, the green shows which regions are back at more typical levels for inventory based on the growth we’ve seen lately. The red shows where things have improved, but are still well below the norm (see graph below):

Here’s what that means for you. Across the board, you have more options now than you would’ve just one year ago. And that’s a really good thing. More choices means it should be a bit easier to find a home you love.

But not all markets are the same – some will take a bit longer to get back to more typical levels. So, lean on a local agent to find out what the inventory situation looks like where you want to live. They’ll be able to tell you how much growth they’ve seen locally and how to tailor your home search based on what’s available in that area. This is just one of the reasons a local agent’s perspective matters.

Bottom Line

Inventory is getting better, but how long it takes to get back to normal is going to be different based on where you’re looking to buy. Talk with a local real estate agent about what’s happening in your local market and how it affects your next move.

What’s one thing you’ve noticed lately that makes the market feel different than it did a year or two ago?

Headlines are saying home prices are starting to dip in some markets. And if you’re beginning to second guess your plans based on what you’re hearing in the media, here’s what you need to know.

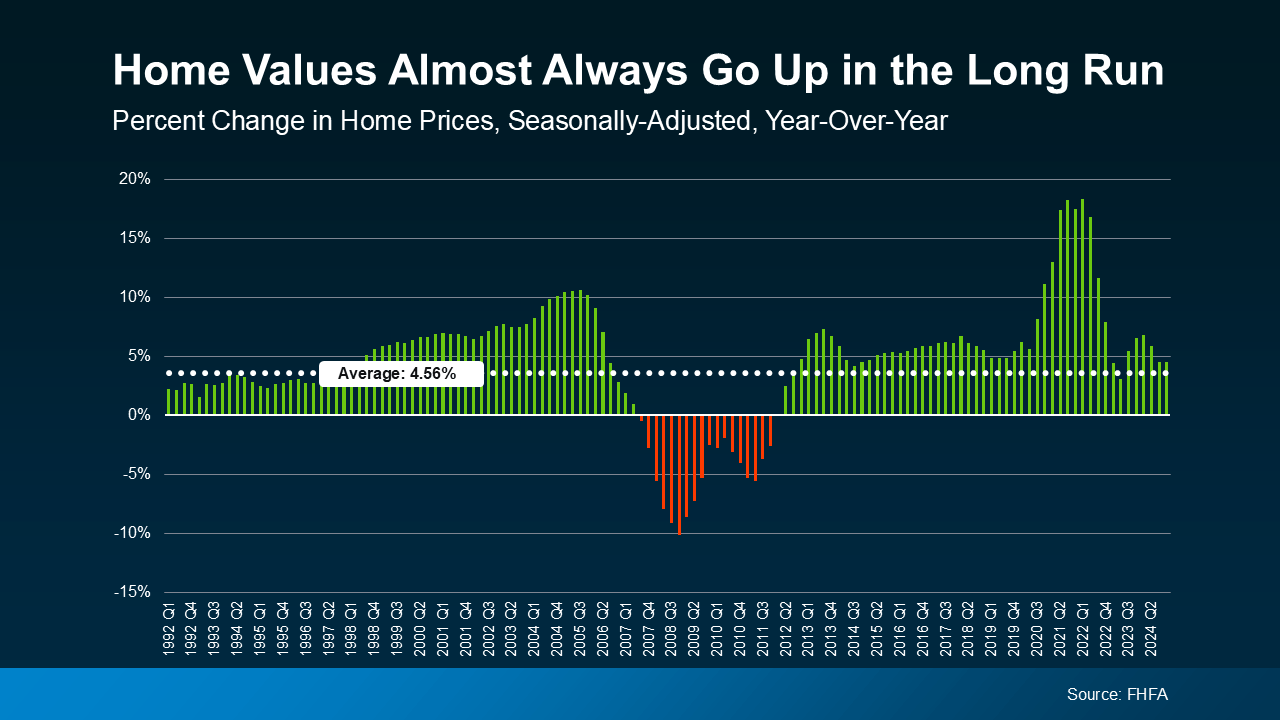

It’s true that a few metros are seeing slight price drops. But don’t let that overshadow this simple truth. Home values almost always go up over time (see graph below):

While everyone remembers what happened around the housing crash of 2008, that was the exception – not the rule. It hadn’t happened before, and hasn’t since. There were many market dynamics that were drastically different back then, too. From relaxed lending standards to a lack of homeowner equity, and even a large oversupply of homes, it was very different from where the national housing market is today. So, every headline about prices slowing down, normalizing, or even dipping doesn’t need to trigger fear that another big crash is coming.

Here’s something that explains why short-term dips usually aren’t a long-term deal-breaker.

What’s the Five-Year Rule?

In real estate, you might hear talk about the five-year rule. The idea is that if you plan to own your home for at least five years, short-term dips in prices usually don’t hurt you much. That’s because home values almost always go up in the long run. Even if prices drop a bit for a year or two, they tend to bounce back (and then some) over time.

Take it from Lance Lambert, Co-Founder of ResiClub:

“. . . there’s the ‘five-year rule of thumb’ in real estate—which suggests that most buyers can buffer themselves from mild short-term declines if they plan to own a property for at least that amount of time.”

What’s Happening in Today’s Market?

Here’s something else to put your mind at ease. Right now, most housing markets are still seeing home prices rise – just not as fast as they were a few years ago.

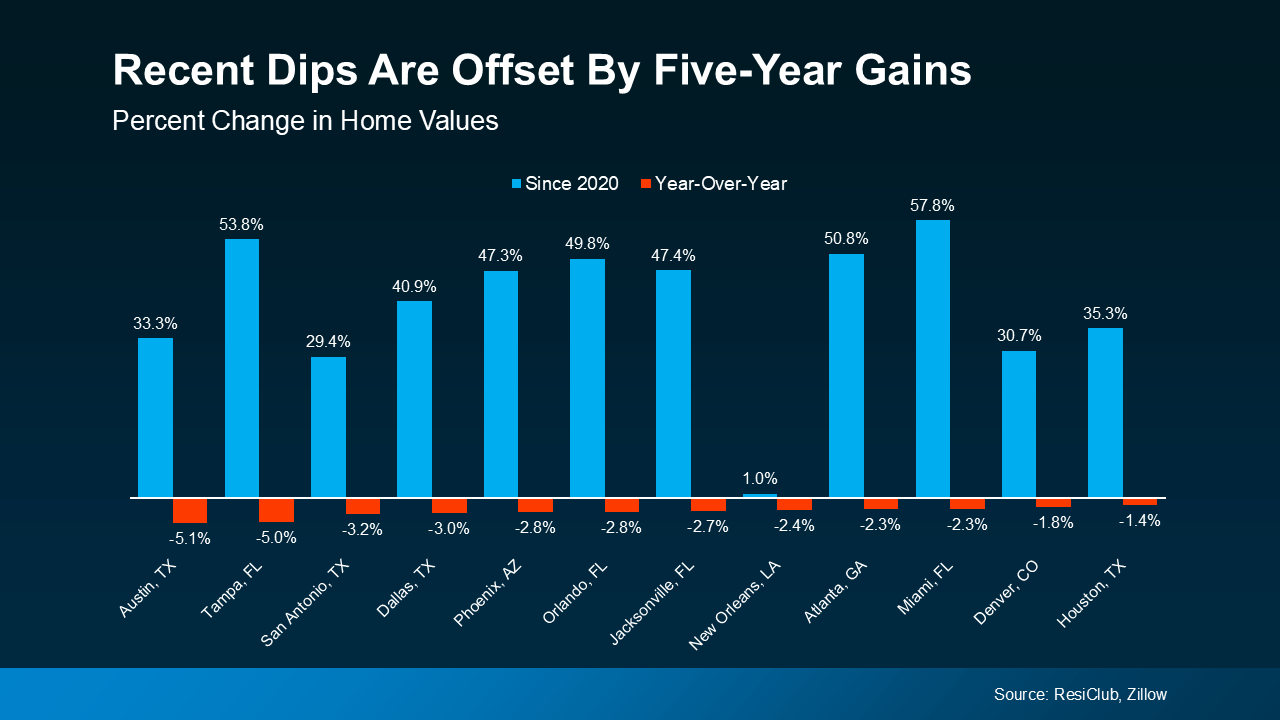

But in the major metros where prices are starting to cool off a little (the red bars in the graph below), the average drop is only about -2.9% since April 2024. That’s not a major decline like we saw back in 2008.

And when you look at the graph below, it’s clear that prices in most of those markets are up significantly compared to where they were five years ago (the blue bars). So, those homeowners are still ahead if they’ve been in their house for a few years or more (see graph below):

The Big Picture

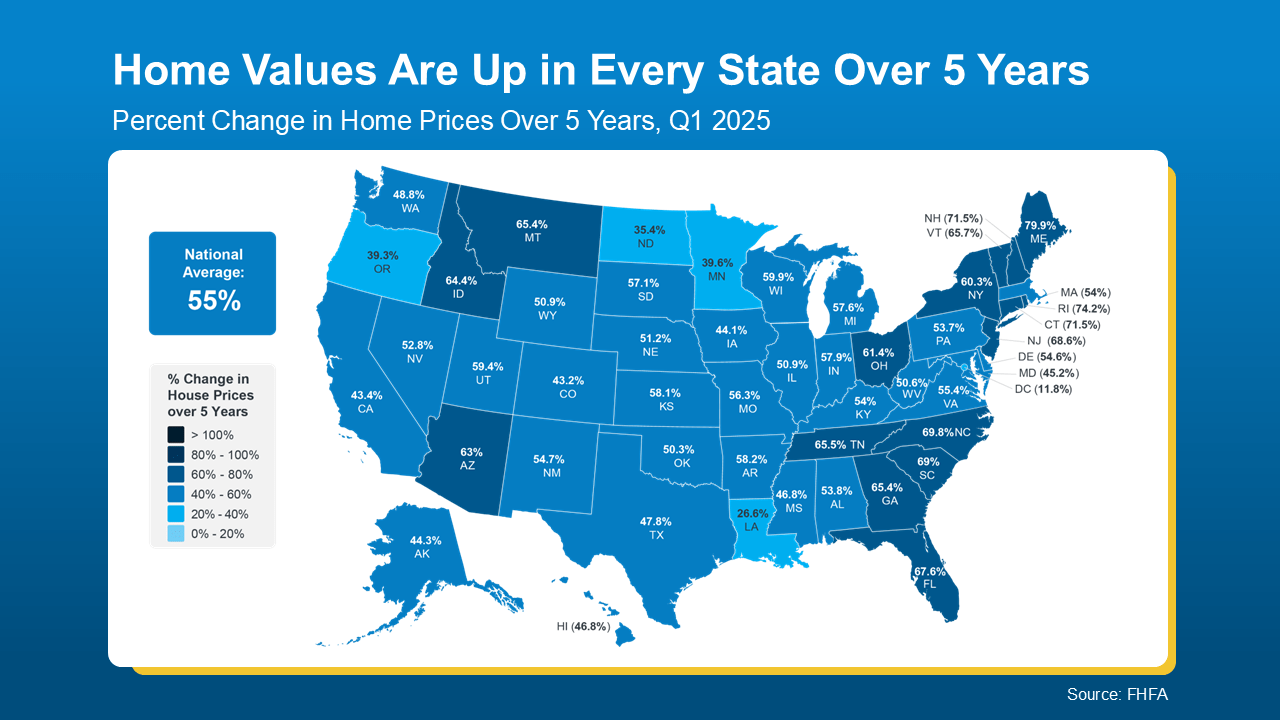

Over the past 5 years, home prices have risen a staggering 55%, according to the Federal Housing Finance Agency (FHFA). So, a small short-term dip isn’t a significant loss. Even if your city is one where they’re down 2% or so, you’re still up far more than that.

And if you break those 5-year gains down even further, using data from the FHFA, you’ll see home values are up in every single state over the last five years (see map below):

That’s why it’s important not to stress too much about what’s happening this month, or even this year. If you’re in it for the long haul (and most homeowners are) your home is likely to grow in value over time.

Bottom Line

Yes, prices can shift in the short term. But history shows that home values almost always go up over five years. So, whether you’re thinking of buying or selling, remember the five-year rule, and take comfort in the long view.

When you think about where you want to be in five years, how does owning a home fit into that picture?

Connect with an agent to discuss how to get there.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better. 4. You Weren’t Willing To Negotiate

4. You Weren’t Willing To Negotiate

The Big Picture

The Big Picture