Why Big Investors Aren’t a Challenge for Today’s Homebuyer

Remember the chatter in the headlines about all the homes big institutional investors were buying? If you were thinking about buying a home yourself, you may have wondered how you’d ever be able to compete with that. Here’s the thing. That’s not the challenge so many people think it is – especially right now.

Let’s break down what’s really going on and why the recent shift in the approach investors are taking could tip the scales in your favor.

Large Investors Are Pulling Back

The truth is institutional investors never represented as big a share of the housing market as people think. And now, they’re backing off even more.

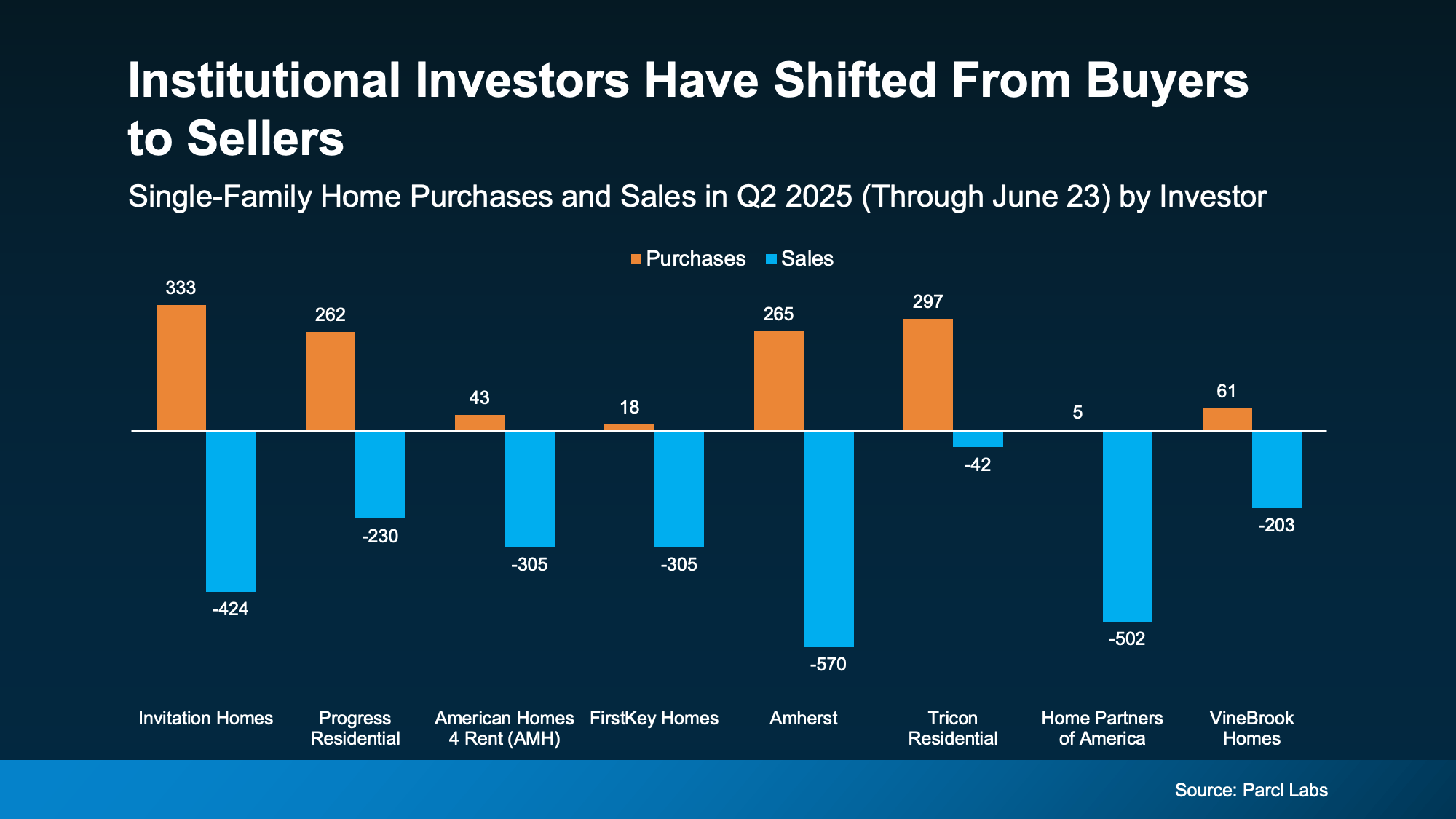

Today, big real estate investors aren’t buying as many homes. In fact, they’re actually selling more than they’re buying.

According to data from Parcl Labs, 6 out of 8 of the largest institutional single-family rental investment companies in America sold more homes than they bought in the second quarter of 2025 (see graph below):

And here’s the stat that really puts it in perspective. According to Dominion Financial, for every home being bought by big investors, about 1.75 are being sold.

What’s Causing Big Investors To Change Course?

The reason institutional investors aren’t buying as many homes now compared to recent years is actually pretty simple. It’s because home values aren’t rising as fast as they were a few years ago, but the costs associated with rental maintenance are.

Since most institutional investors buy homes to rent them out, those higher costs eat into their margins. Remember, to investors, homebuying is a business.

But you’re not buying a home just for this year or next. You’re buying a place to build a life, and that’s a long-term play.

Historically, home values tend to rise over time. So, while investors may be sidelined by what’s happening right now, you’re in a different position entirely. You have the chance to buy while competition is lower and benefit from potential long-term price appreciation – something most investors are choosing not to wait for as they focus on shorter-term returns.

What Does All This Mean for You?

According to a recent survey, about 55% of real estate investors have no plans to grow their rental portfolios now or in the near future. With big investors stepping back, that means less competition from deep-pocketed buyers. And since they’re adding to today’s for-sale inventory, it also creates more options for you.

Bottom Line

If you’ve been holding off on buying, now might be the time to take another look. Connect with a local real estate agent so you can get expert guidance on what’s available and what might be a good fit for you.

What kind of home would you be excited to make yours this year?

The Big Picture

The Big Picture