What Happens to the Housing Market When the Economy Slows Down?

There’s a lot of noise out there about what an economic slowdown could mean for the housing market. And if it leaves you feeling a little uneasy, you’re not alone. But here’s the thing.

If you’re worried about what a potential recession could mean for the value of your home, or your homebuying power, your trusted REMAX® agent is here to help set the record straight. You don’t have to fear the market when you understand what the data actually shows.

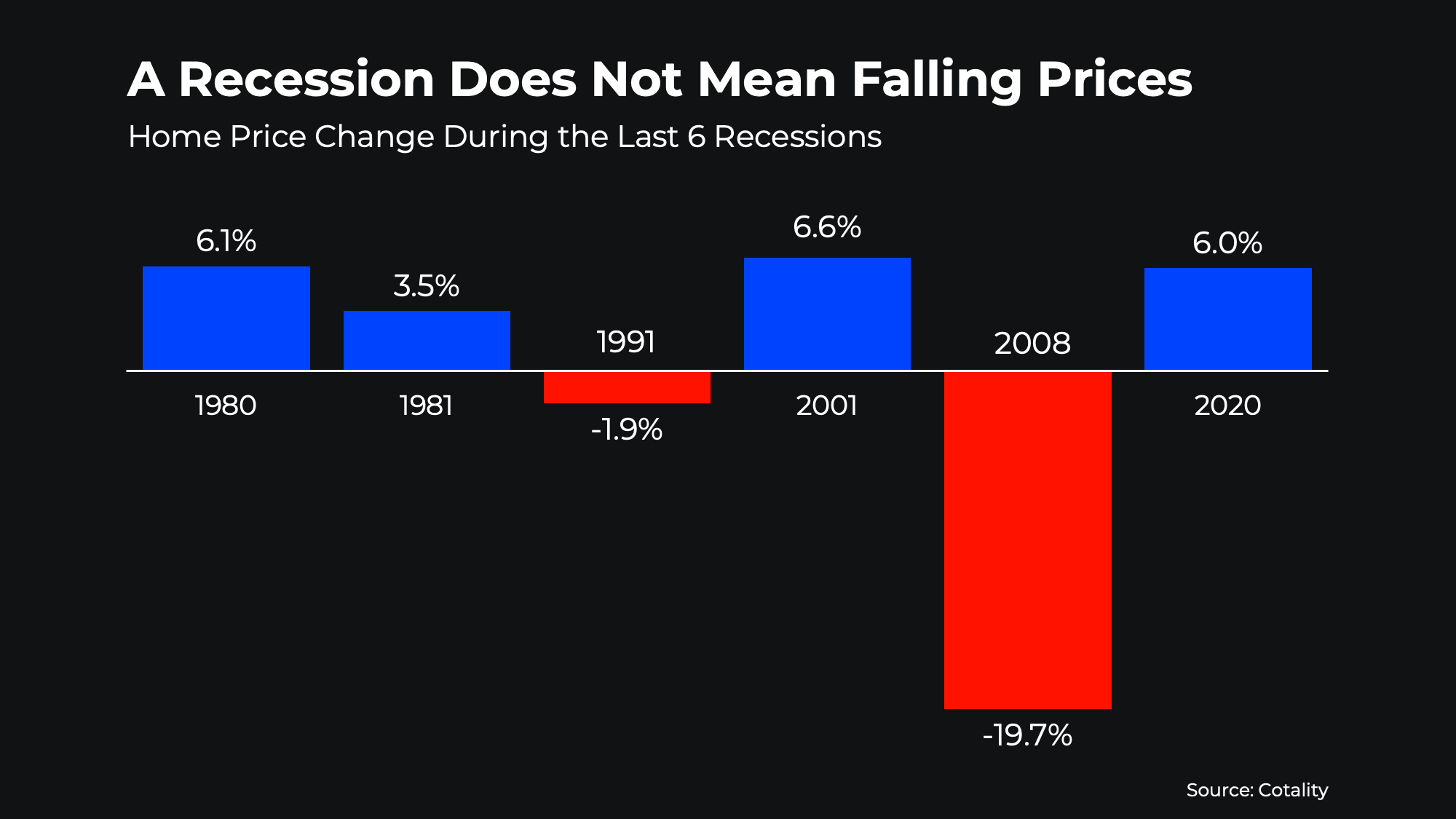

A Recession Doesn’t Automatically Mean Home Prices Will Fall

It’s easy to assume that if the economy slows down, home prices will fall. You might remember what happened in 2008. But the truth is: the housing crash of 2008 was an exception — not the rule.

It hadn’t happened before. And it hasn’t happened since. But what made 2008 so different? It was a flood of oversupply and very different lending standards. And everyone remembers how painful that time was.

Today, lending is much tighter, and even with inventory rising, the overall number of homes for sale remains well below normal levels. That keeps upward pressure on prices — and it keeps prices from falling significantly on a national level. And while prices are moderating in some markets today, a significant crash is unlikely.

In fact, according to data from Cotality, in four of the last six recessions, home prices actually went up (see graph below):

Don’t let fear of a recession make you assume prices are about to fall dramatically.

Don’t let fear of a recession make you assume prices are about to fall dramatically.

And since prices usually follow the path they’re already on, in most markets they should rise, not fall, in the days ahead. The rise just may slower, or even flat, but certainly not a crash.

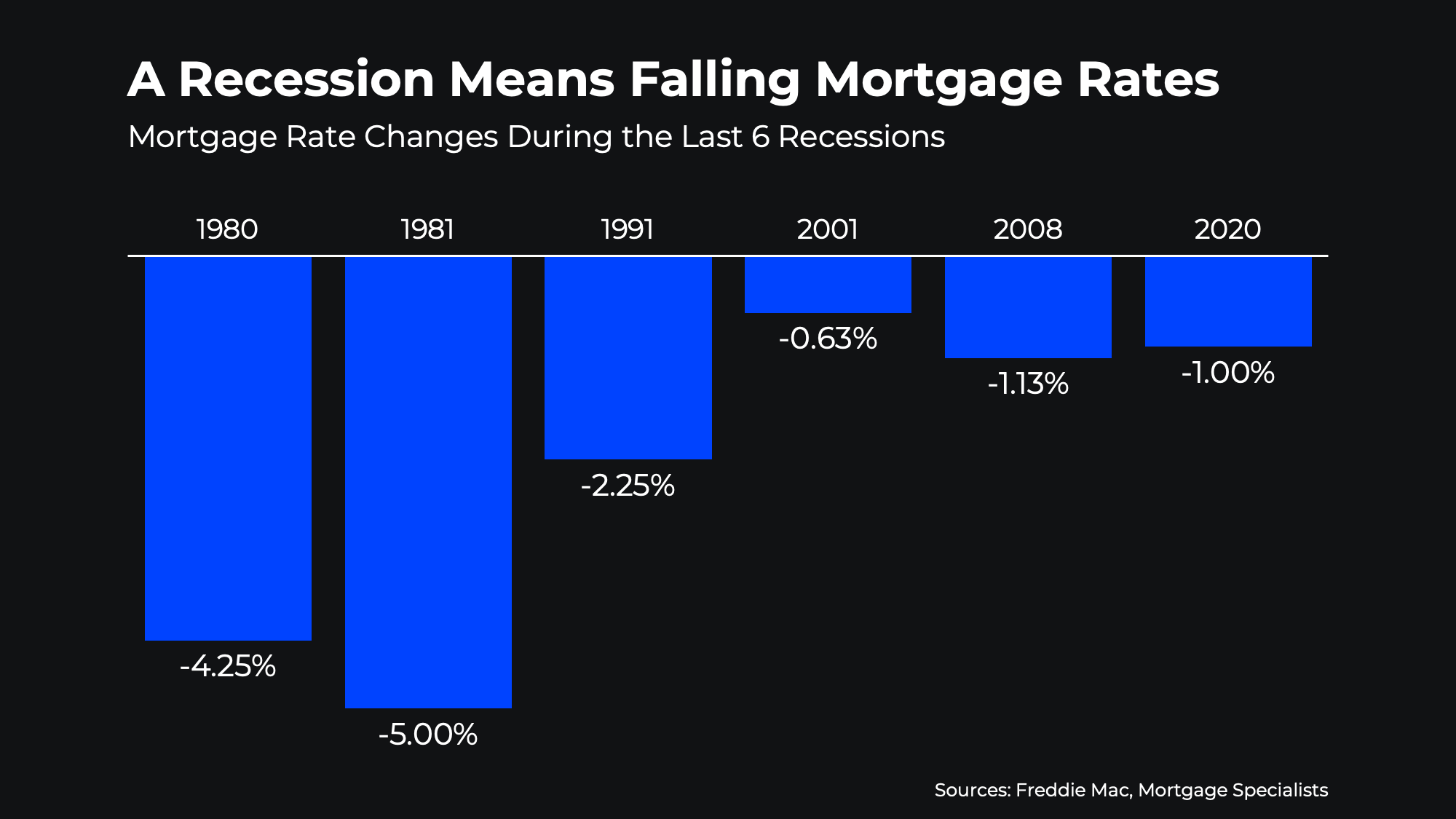

Mortgage Rates Typically Decline During Recessions

Another important pattern you should know? Mortgage rates usually fall when the economy slows down.

Looking at the data for the last six recessions, mortgage rates came down each time — helping boost buyer purchasing power, even during tougher economic periods (see graph below):

If a recession does happen, history suggests you could see some relief in mortgage rates. However, it’s important to stay realistic. While a dip is possible, we’re unlikely to return to the ultra-low 3% rates seen in 2020 and 2021.

If a recession does happen, history suggests you could see some relief in mortgage rates. However, it’s important to stay realistic. While a dip is possible, we’re unlikely to return to the ultra-low 3% rates seen in 2020 and 2021.

Bottom Line

Economic shifts are part of the cycle, but they don’t have to derail your plans to buy or sell a home. Don’t let fear be the thing that keeps you from your next move.

Instead, lean on facts to guide your decisions. And your trusted REMAX agent is the perfect person to make sure you have the information you need to feel confident moving forward.

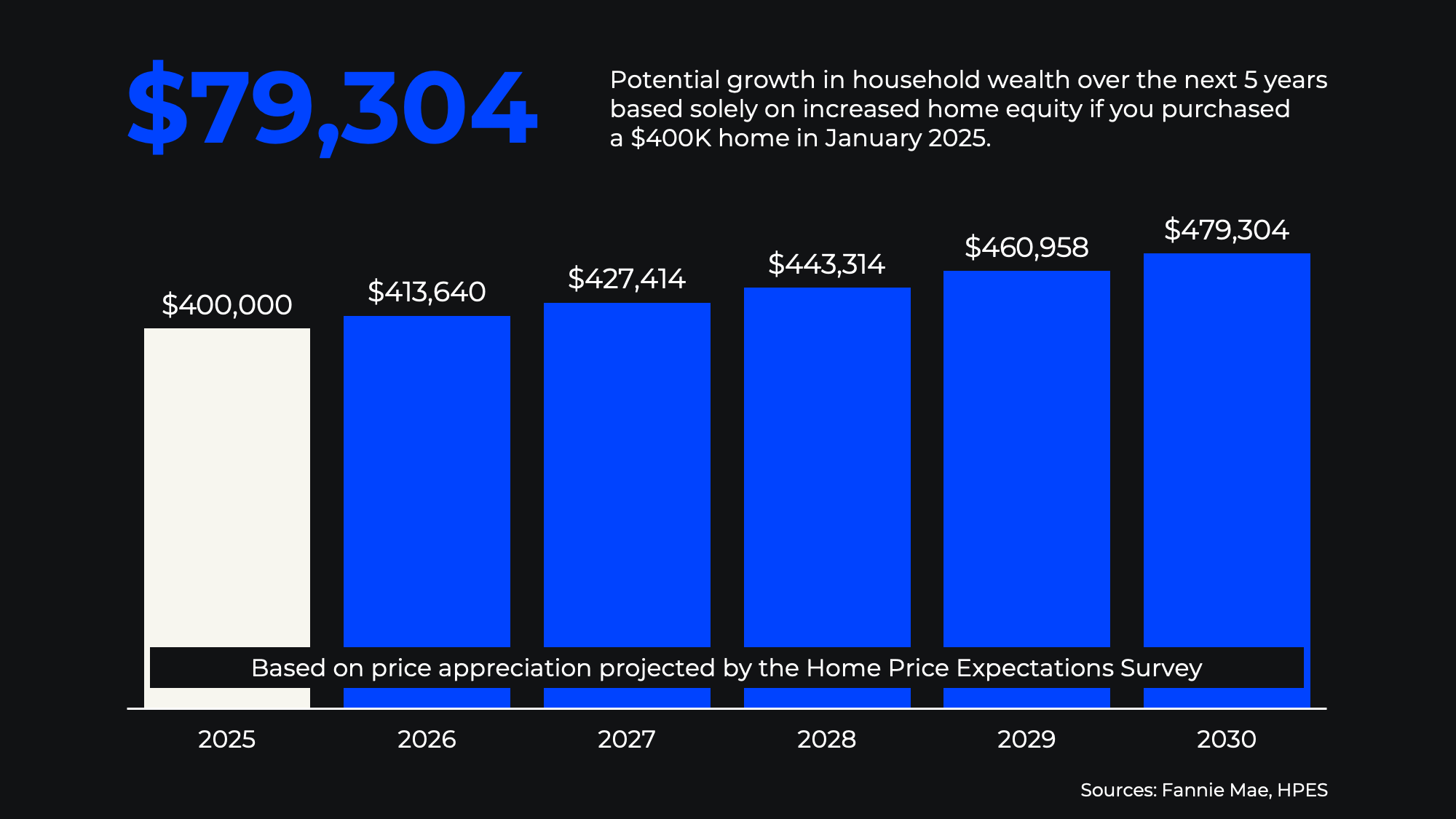

That’s $80K you could be gaining in home value — or losing out on if you keep sitting on the sidelines.

That’s $80K you could be gaining in home value — or losing out on if you keep sitting on the sidelines.