The right agent doesn’t just list your house – they help you sell smarter, faster, and with fewer surprises.

With an agent’s help, you’ll know what’s happening in your local market and how to price your house right. You’ll feel confident filling out complex legal documents and at the negotiation table. And that’s priceless.

Connect with an agent so you have that expertise on your side.

Here’s something you need to know. The housing market is getting back to a healthier, more normal place. And even though it may not sound like it, this shift is actually a good thing.

It’s what you should expect. It’s just that our expectations have been skewed by the intense seller’s market over the past few years.

But what you need to remember is: there’s still plenty of opportunity to be had if you’re thinking about selling – whether that’s next month or next year. You just need to stay up to date on what’s happening in the market, and have a strategy that matches the moment. Here’s your update.

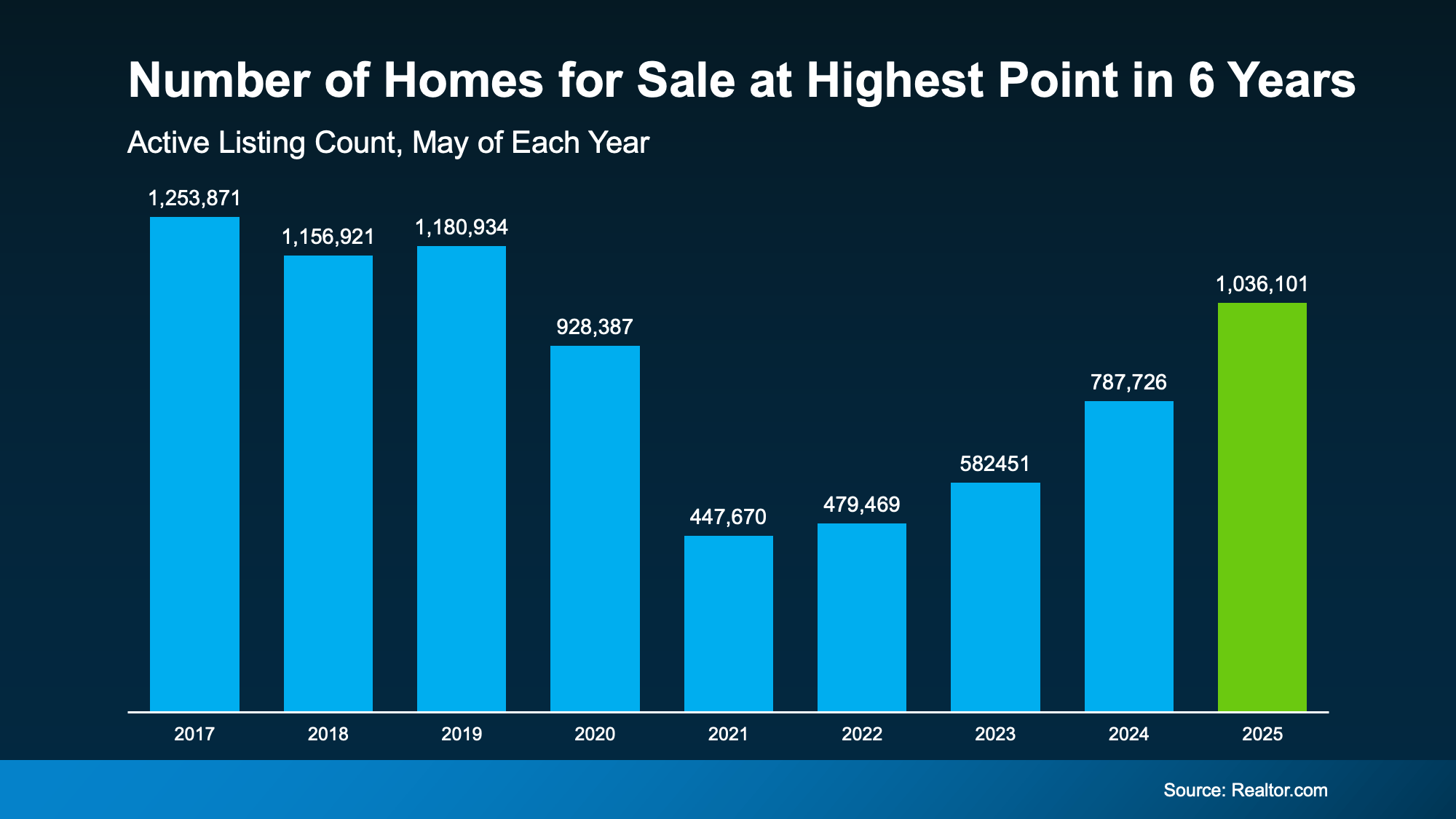

1. Inventory’s Up. Buyer Power Is Coming Back.

According to the latest data, the number of homes for sale is rising back toward more normal levels (see graph below):

But inventory growth is going to vary a lot based on where you live.

If you’re in a market where the number of homes for sale is back to normal, buyers may have more sway than you’d expect. That doesn’t mean buyers have all the power – it just means they have more choices, so your home has to stand out.

But if you live where inventory is still pretty limited, you may see more buyers competing for your house.

No matter where you are, the key is to work with a pro who can help you adjust your game plan for your local market.

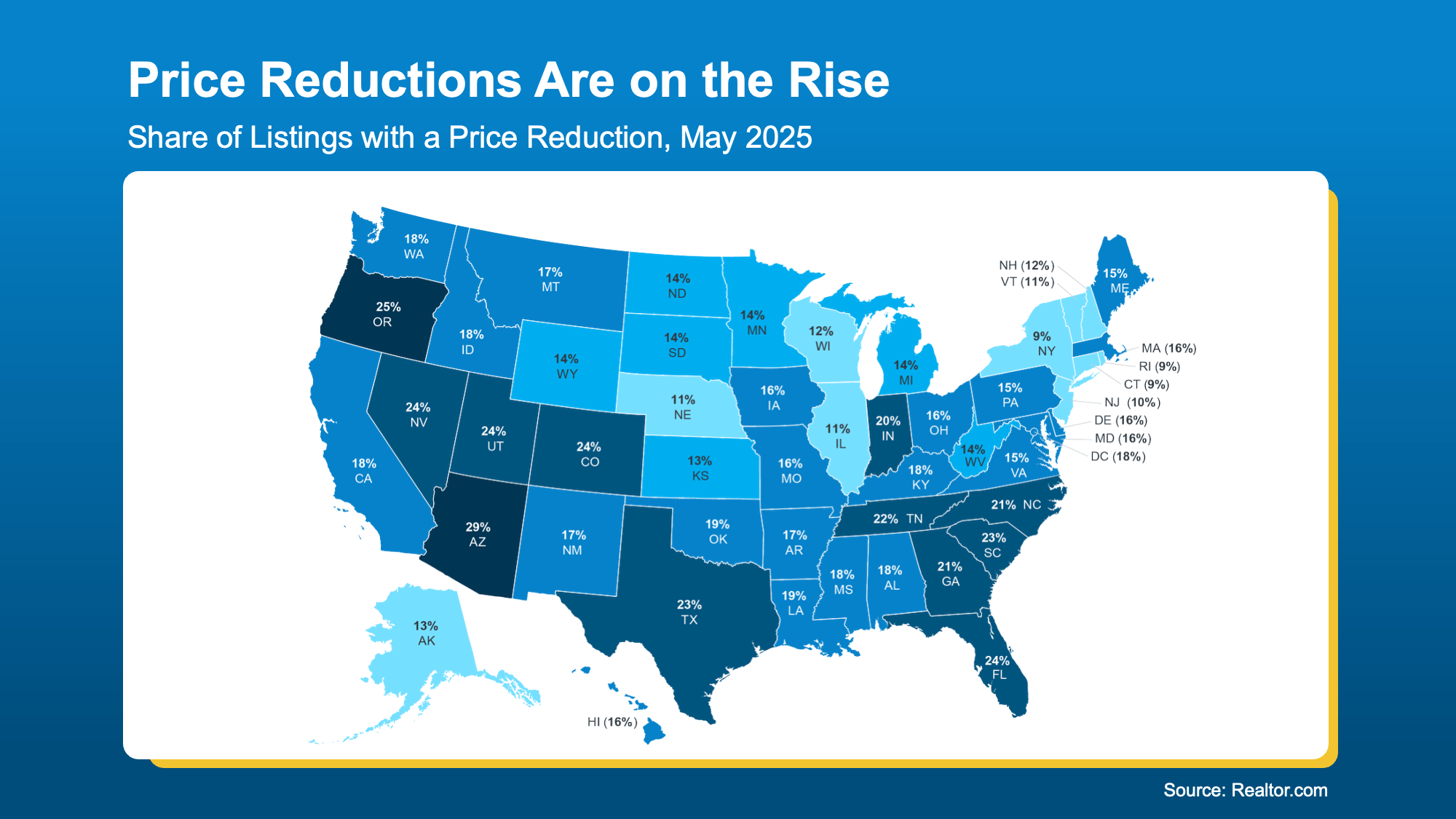

2. The Right Price Matters More Than Ever

With more homes to choose from, today’s buyers are quick to skip over homes that feel overpriced. That’s why pricing your house right is the secret to selling quickly and for top dollar. That’s a pointRealtor.com really drives home:

“ . . . a seller listing a well-priced, move-in ready home should have little problem finding a buyer.”

Miss the mark, though, and you may have to backtrack. Today, about 1 in 5 sellers (19.1%) are reducing their asking price to attract buyers (see map below):

Here’s how to avoid being one of those sellers who has to reduce their asking price. Danielle Hale, Chief Economist at Realtor.com, says:

“The rising share of price reductions suggests that a lot of sellers are anchored to prices that aren’t realistic in today’s housing market. Today’s sellers would be wise to listen to feedback they are getting from the market.”

The best way to get that information? Lean on your local agent. They have the expertise to set a price that sells in any market. Because if your price isn’t compelling, it’s not selling.

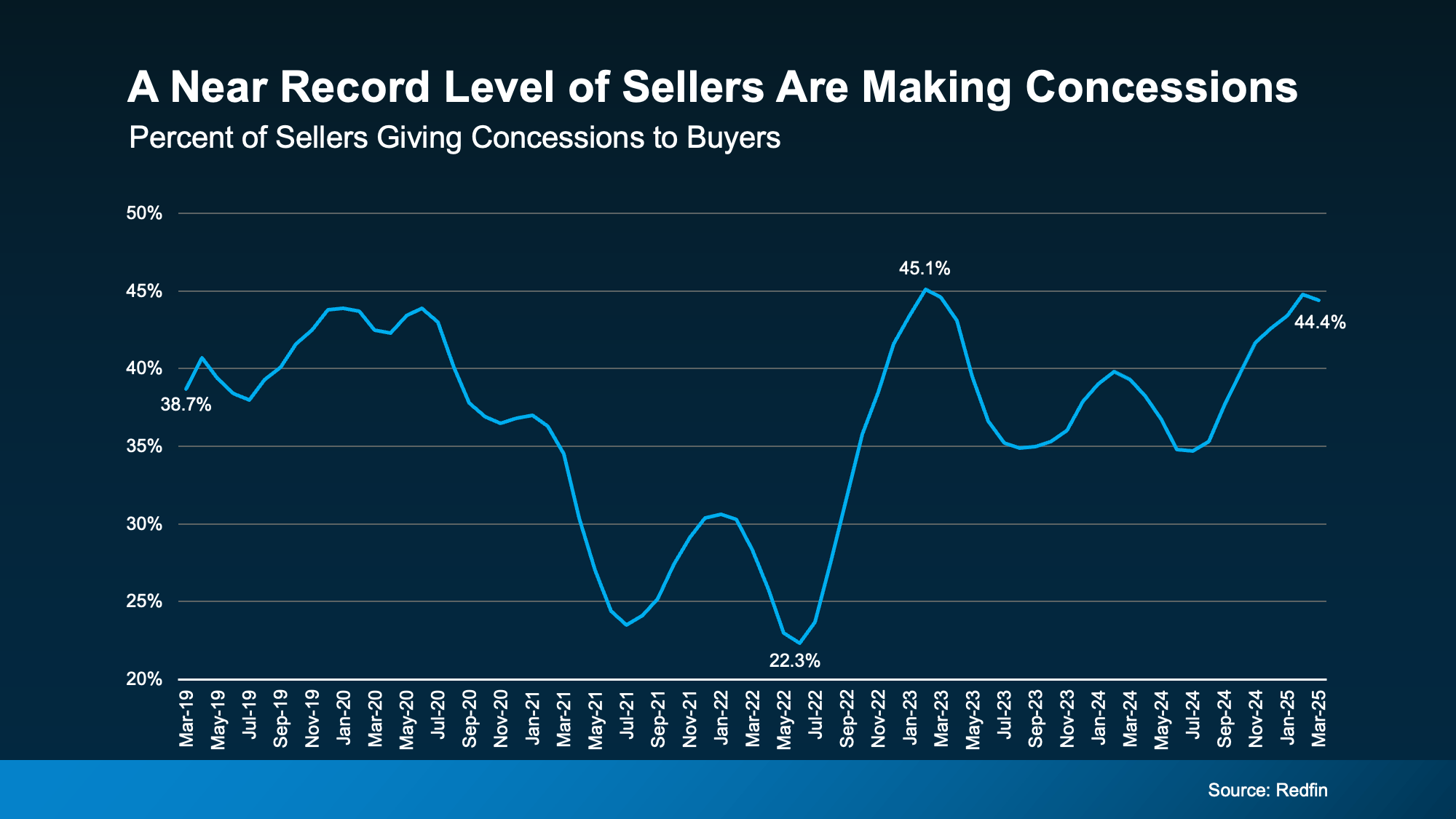

3. Flexibility Wins Negotiations

Gone are the days of buyers waiving inspections and appraisals just to get a deal done. Now, because they have more homes to choose from, buyers are able to ask for things like repairs, credits, and help with closing costs. And data from Redfin shows nearly44.4% of sellers are willing to negotiate (see graph below):

The takeaway? This isn’t a bad market. It’s just a different one. And it’s in line with more normal years in the housing market, like back in 2019. The savviest sellers are the ones taking advantage of every opportunity to work with buyers and make their house shine.

And it’ll help if you think of concessions as tools, not losses. Use them to bridge gaps, sweeten deals, and get across the finish line.And don’t stress. Since prices went up roughly 55% over the past five years, you’ve got plenty of room to make a concession or two and still come out ahead.

Just be sure to work with your agent to understand which concessions could be the key to sealing the deal.

Bottom Line

Sellers who are going to succeed in the weeks and months ahead are the ones who understand this market shift and lean into it with the right expectations and the right strategy.

Connect with a local agent and talk about what’s working in your area right now – and how to make those wins work for you, too – whenever you’re ready to make a move.

When your house doesn’t sell, it doesn’t just feel frustrating – it feels personal. You put time, money, and emotional energy into this move. You told your friends and family it was happening. And now that your listing has expired without a buyer? You’re left feeling stuck, and maybe even a little embarrassed.

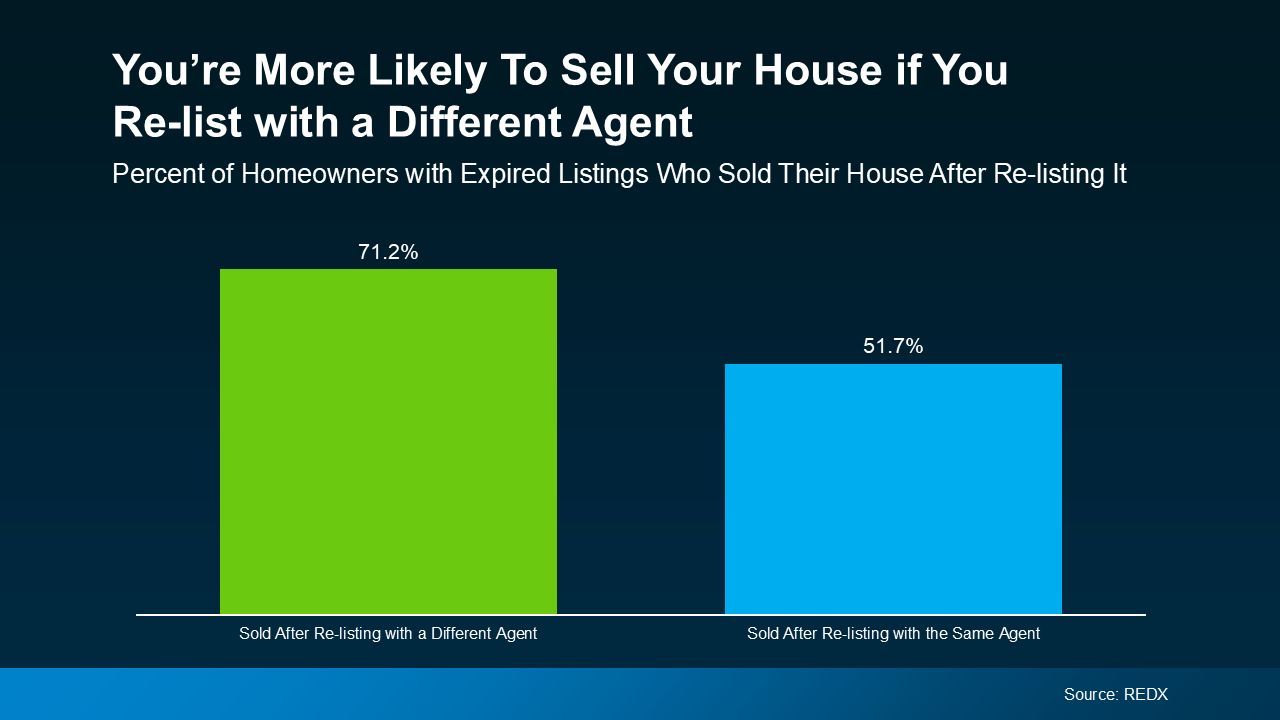

And here’s what most agents won’t tell you. Over 70% of homeowners who re-list with a different agent sell their house.

Re-list with the same agent? That stat drops to only 50%, according to the latest data from REDX. That’s like leaving the fate of your sale to a coin toss. And that’s not good enough.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better.

Same house. Different strategy. Completely different results.

Let’s break down what might’ve gone wrong – and how a fresh perspective can help you have a winning strategy this time.

1. It Was Priced Too High

Today, homebuyers are feeling the squeeze of higher mortgage rates, so even a slightly overpriced home will get overlooked. And once your listing starts to go stale, it’s hard to regain momentum.

Missing the mark on pricing is a costly mistake – and too many homeowners are doing that very thing right now.

What we need to do now: We need to analyze the latest sales in your area to make sure you’re hitting the right number. This includes taking a hard look at real-time buyer behavior, and any feedback you got from open houses or showings your first time around. Pricing at, or even just below, current market value is a winning play because it drives more buyers to your listing – and that amps up the competition for your home.

2. It Didn’t Show Well

You only get one shot at a first impression. If the listing photos didn’t pop, the house wasn’t staged well, or it wasn’t updated, most buyers will skip over it without ever scheduling a showing. And even if buyers did show up, small things like scuffed walls, outdated light fixtures, or a wobbly doorknob can turn them away.

What we need to do now: Let’s walk through your house withfresh eyes to see if there are any areas that may have been sticking points inside and out. Sometimes taking down old drapery, some light staging, or even a fresh coat of paint can completely change how a buyer feels about the home.

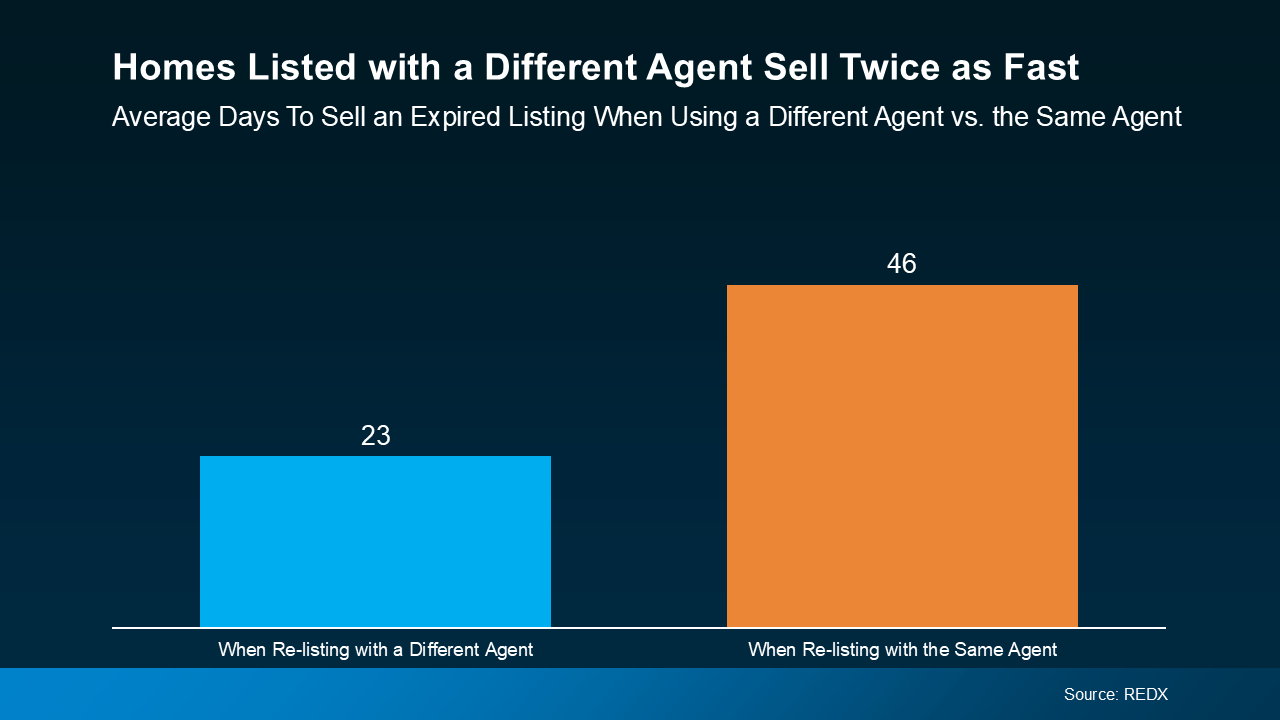

3. It Didn’t Get the Right Exposure

If your home didn’t sell, chances are it wasn’t getting the visibility it deserved. Generic flyers and a few online photos aren’t enough anymore. Today’s top agents are using highly targeted digital marketing, social media strategies, custom video content, and more to get your listing in front of the right buyers at the right time.

What we need to do now: We have to do more than just put your house online and hope it sells. Together, we can come up with a real plan to maximize its exposure. With the right pricing, staging, and marketing, your house will sell quickly. Here’s a real-world example (see graph below):

4. You Weren’t Willing To Negotiate

In this market, sellers who aren’t open to negotiating on things like closing costs, inspection repairs, or other concessions are often left behind. And if your last agent didn’t set that expectation with you, that’s a real shame.

What we need to do now: Be willing to meet buyers where they are. The goal is to get the deal done – and sometimes that means getting creative to help buyers cross the finish line. Home values have increased by over 55% over the last five years, so you likely have enough wiggle room to offer some perks without sacrificing your bottom line.

Bottom Line

If your house didn’t sell and your listing has expired, you don’t need to give up. You just need a better plan. And maybe, a better partner.

Over 70% of homeowners who switch agents sell their house the second time. That’s not a coincidence. That’s strategy.

If you’re ready for a proven approach, talk to a local agent so you know what to do differently – and why doing different things actually works. It’s time to get your move back on track.

Now that buyers have more options for their move, you need to be a bit more intentional about making sure your house looks its best when you sell. And proper staging can be a great way to do just that.

What Is Home Staging?

It’s not about making your house look super trendy or like it belongs in a magazine. It’s about helping it feel welcoming and move-in ready, so it’s easy for buyers to picture themselves living there.

It’s important to understand there’s a range when it comes to staging. It can include everything from simple tweaks to more extensive setups, depending on your needs and budget. But a little bit of time, effort, and money invested in this process can really make a difference when you sell – especially in today’s market.

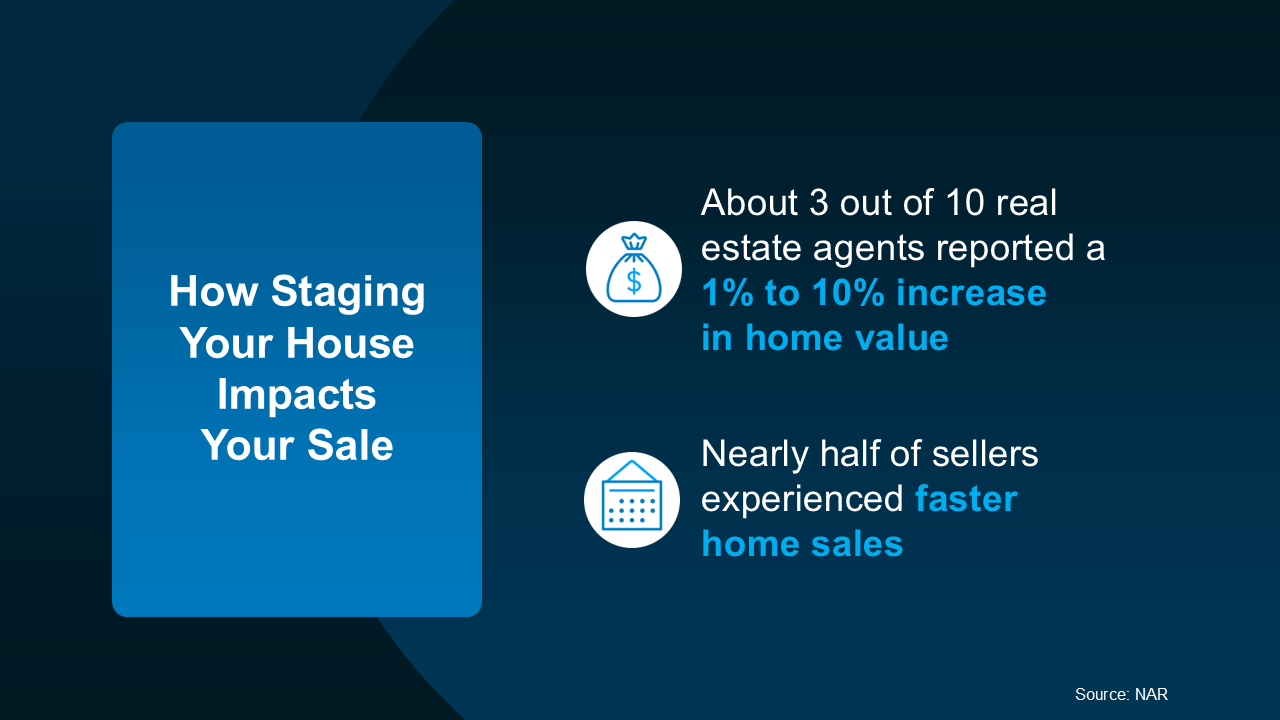

A study from the National Association of Realtors (NAR) shows staged homes sell faster and for more money than homes that aren’t staged at all (see below):

Which Rooms Matter Most?

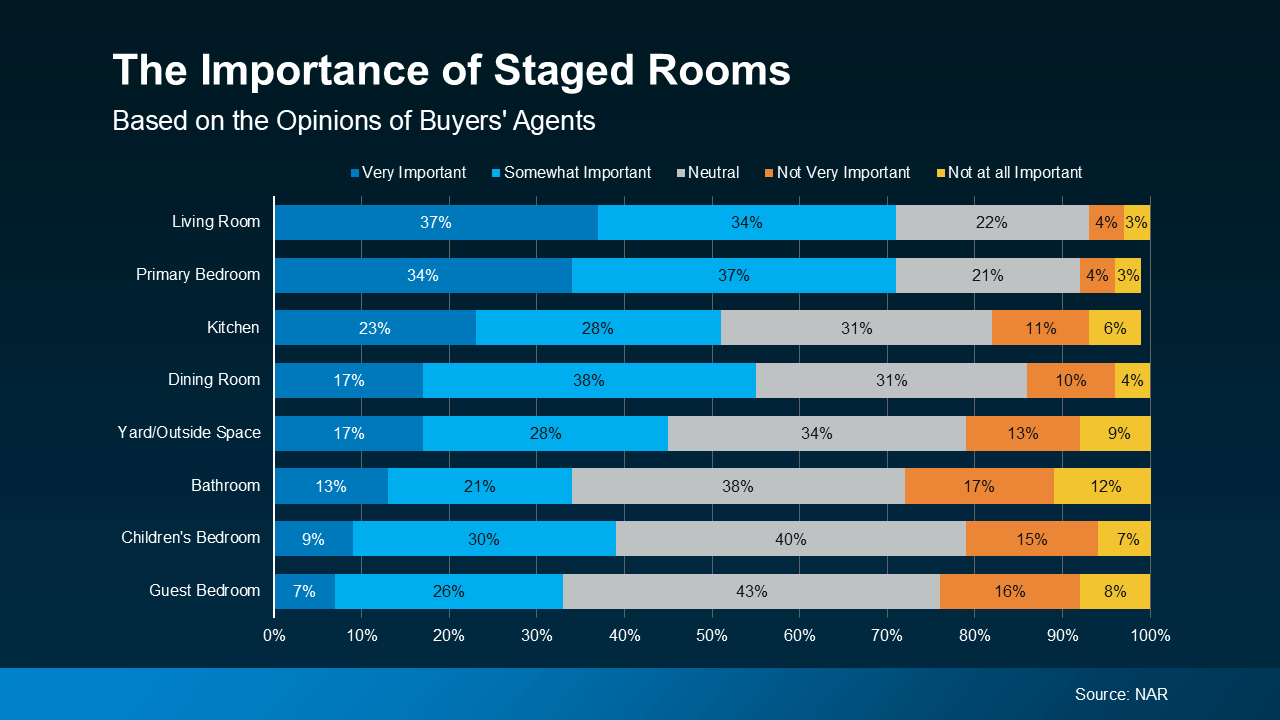

The best part is, odds are you don’t have to stage your whole house to make an impact. According to NAR, here’s where buyers’ agents say staging can make the biggest difference (see graph below):

As you can see, agents who talk to buyers regularly agree, the most important spaces to stage are the rooms where buyers will spend the most time, like the living room, primary bedroom, and kitchen.

While this can give you a good general idea of what may be worth it and what’s probably not, it can’t match a local agent’s expertise.

How an Agent Helps You Decide What You Need To Do

Agents are experts on what buyers are looking for where you live, because they hear that feedback all the time in showings, home tours, walkthroughs, and from other agents. And they’ll use those insights to give their opinion on your specific house and what areas may need a little bit of staging help, like if you need to:

Declutter and depersonalize by removing photos and personal items

Arrange your furniture to improve the room’s flow and make it feel bigger

Add plants, move art, or re-arrange other accessories

A lot of buyers can use the agent’s know-how as the only staging advice they need. But, if your home needs more of a transformation, or it’s empty and could benefit from rented furniture, a great agent will be able to determine if bringing in a professional stager might be a good idea, too. Just know that level of help comes with a higher price tag. NAR reports:

“The median dollar value spent when using a staging service was $1,500, compared to $500 when the sellers’ agent personally staged the home.”

A local agent will help you weigh the costs and benefits based on your budget, your timeline, and the overall condition of your house. They’ll also consider how quickly similar homes are selling nearby and what buyers are expecting at your price point.

Bottom Line

Staging doesn’t have to be over-the-top or expensive. It just needs to help buyers feel at home. And a great agent will help you figure out the level of staging that makes the most sense for your goals.

Which room in your house do you think would make the biggest impression on a buyer?

Get an agent to walk through your home with you and go over what will make your house stand out.

But inventory growth is going to

But inventory growth is going to

The takeaway? This isn’t a bad market. It’s just a different one. And it’s in line with more normal years in the housing market, like back in 2019. The savviest sellers are the ones taking advantage of every opportunity to work with buyers and make their house shine.

The takeaway? This isn’t a bad market. It’s just a different one. And it’s in line with more normal years in the housing market, like back in 2019. The savviest sellers are the ones taking advantage of every opportunity to work with buyers and make their house shine.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better.

REDX data also shows that only 1 in 3 homeowners with expired listings actually make that change. That means most sellers either give up or repeat the same mistakes, so they get the same disappointing outcome. You deserve better. 4. You Weren’t Willing To Negotiate

4. You Weren’t Willing To Negotiate